Hong Kong’s housing market has continued to rise since July 2003, a bull cycle that has many similarities with the previous one that occurred between September 1984 and October 1997.

One common feature of the two bull cycles is that both started after a steep slump of 60-70 percent.

In early 1980s, housing prices started to decline amid political uncertainties, and reversed the downward course only after falling almost by a cumulative 70 percent.

Before the current bull cycle began, Hong Kong went through Asian financial crisis in 1997, the bursting of the internet bubble in 2000 and the SARS outbreak in 2003. Home prices also tumbled nearly 70 percent during the period.

As can be observed, the housing market apparently often goes through a deep correction before a sustained rally begins.

The second thing that is common between the two property booms is that housing prices never showed a correction bigger than 20 percent during the period.

The first bull cycle had an accumulative rally of 935 percent, compared with 448 percent in the current cycle.

However, the inflation-adjusted housing price soared 292 percent in the first bull cycle, and close to 278 percent in the current cycle.

Yet there is one notable difference. In the 1988-1997 bull run, big apartments were leading the charge, whereas this time, the small units are outperforming.

The first bull cycle lasted 158 months or 13.2 years, while the second one has already extended for 165 months or 13.75 years as of March.

Does that mean the bull cycle is ending? There is no simple answer.

It is, however, noteworthy that external factors played a key role in the market’s ups and downs.

The previous bull market was killed by the Asian financial crisis, and this time, property prices were to a certain extent buoyed by the influx of capital.

The trigger that will end the current bull market may also be an external shock.

Translation by Julie Zhu

香港樓市兩大上升周期比對

呂梓毅

信報首席經濟及策略師

香港回歸20年,近日媒體多了有關回歸前後經濟和股市等不同範疇的比對和分析。雖然目前樓價尚未見頂(繼續尋頂中?),但自2003年7月至今的樓市大升浪,其實與1984年9月至1997年10月的上升大周期,有不少異同及有趣的地方,今期我們與讀者探討這課題。

本文將探討本港樓市的兩個上升大周期,分別是1984年9月至1997年10月的升浪(下簡稱:「上升大周期1」)和2003年7月至今(升浪尚未完結)的上升周期(下簡稱:「上升大周期2」;【圖1】 上半部)。為何自1980年至今逾36年的歲月中,筆者只把香港樓市劃分為兩個上升大周期呢?

上半部)。為何自1980年至今逾36年的歲月中,筆者只把香港樓市劃分為兩個上升大周期呢?

大升前皆現深度下挫

主要原因有二,在樓價開展上升大周期前,樓市同樣經歷逾六成大幅下瀉的洗禮。在八十年代初,受香港前途問題所衝擊,香港樓價拾級而下;從樓市在6年或以內的最大跌幅可見,樓價期內最多跌達三成。不過,若連同期內美元兌港元滙價(當時尚未有聯滙)曾急插近四成,樓價當時累計下挫接近七成,才開展「上升大周期1」。

至於開始「上升大周期2」之前,香港經歷1997/98年亞洲金融風暴、2000年科網股爆破和2003年沙士(SARS),香港樓價最大的累計跌幅同樣接近七成;由此可見,樓市在出現「上升大周期1」和「上升大周期2」之前,均出現甚具深度的下跌,由極低殘的位置起步回升(【圖1】下半部)。

除此之外,在樓市處於「上升大周期1」和「上升大周期2」期間,樓價同樣未曾出現過逾兩成的大調整轉向訊號。基於以上兩項因由,筆者把樓市自1980年至今的發展,界分為兩個獨特的上升大周期(雖然「上升大周期2」尚未確認完結)。以下是這兩個樓市大周期的異同:

上升幅度和上升周期維持的時間。僅從上升幅度角度看,「上升大周期1」的累計升幅高達935%(或按年升19.4%),遠遠拋離「上升大周期2」(截至今年3月底為止)累計上升448%(或按年升13.2%)。不過,若從實質(即扣除通脹)樓價的角度看(以今天購買力計算),樓價在「上升大周期1」和「上升大周期2」的累計升幅便分別達292%和278%,即兩者累計升幅頗為接近【圖2】 。事實上,樓價若從現水平再升約3.5%,「上升大周期2」便可平了「上升大周期1」期內的上升幅度。

。事實上,樓價若從現水平再升約3.5%,「上升大周期2」便可平了「上升大周期1」期內的上升幅度。

今輪升勢已維持逾13年

至於上升周期涉及的時間方面,整個「上升大周期1」長達158個月或13.2年;反之,截至今年3月底為止,「上升大周期2」已達165個月或13.75年,暫時較「上升大周期1」的時間略長;惟由於「上升大周期2」尚未完結,是次上升周期將會相較「上升大周期1」涉及時間長多少才完結,還有待觀察。

順帶一提,目前樓價相對1997年高位高約85%,或每年升約3.2%,相當於期間香港名義GDP增長速度;惟若用目前的購買力計算,升幅則只有50%,平均每年升約2.1%。

受惠單位種類。若從實質樓價的升幅角度看,整體樓市在這兩個大周期的升幅相若,惟受惠單位種類卻截然不同。從A類單位(實用面積達40平方米以下)與D及E類單位(實用面達100至159.9平方米及160以上平方米)比率可見(下簡稱「面積比率」;註:比率上升,代表細單位樓價跑贏大單位;反之亦然),踏入「上升大周期1」初至中期,面積比率於高位反覆回升;惟於周期較後時間,有關比率則從高位顯著回落,並明顯較上升周期初期為低。

若用文字解說,踏入「上升大周期1」初中期,細單位面積的樓價表現相對較佳(也許受港人移民潮的影響,令較大面積類別單位初期沽壓較大);惟周期的較後時間,炒風熾熱,大面積單位樓價開始發力, 並且顯著跑贏細單位。簡言之,「上升大周期1」升勢受惠的單位種類主要是大型單位【圖3】。

並且顯著跑贏細單位。簡言之,「上升大周期1」升勢受惠的單位種類主要是大型單位【圖3】。

97年升浪 大單位跑贏

至於「上升大周期2」,初期面積比率大致低位持平,即踏入「上升大周期2」的初期,大、小單位樓價表現相若。不過,在金融海嘯後至今,面積比率卻輾轉回升,並且攀升至1993年以來的高位,顯示隨後細單位顯著跑贏大單位;而這現象相信這與政府辣招有一定關係。

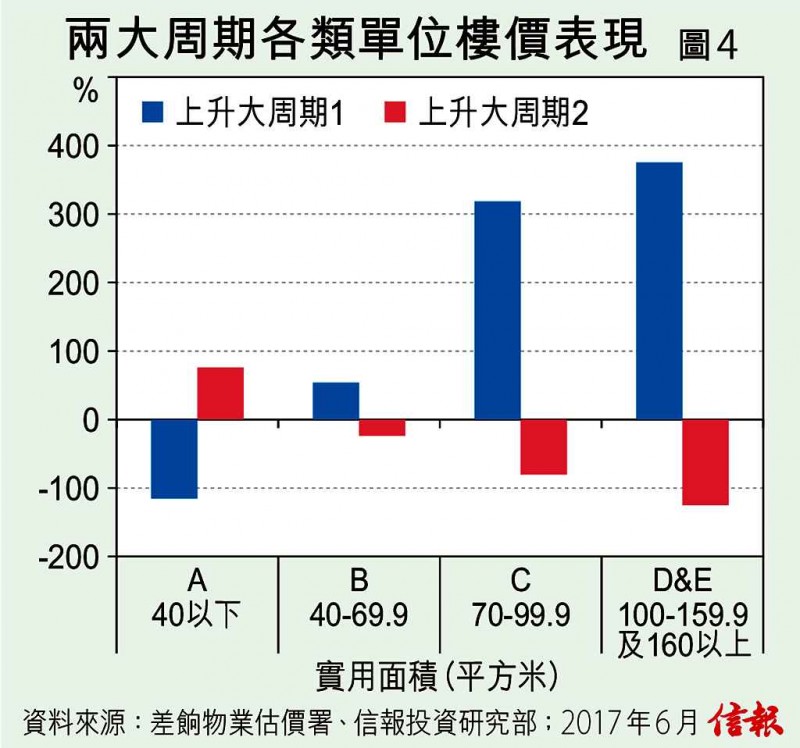

換言之,「上升大周期1」期間,大型單位表現相對突出;反之,「上升大周期2」,小型單位表現則較佳。事實上,若然我們計算A、B、C、D及E不同類別單位,在大周期1和2與整體樓價升幅差距,可發現在「上升大周期1」內,單位面積愈大,跑贏整體價格表現的幅度便愈大;反之,在「上升大周期2」期間, 單位面積愈小,跑贏整體價格表現的幅度便愈大【圖4】。

總括而言,在過去逾30多年裏,香港樓市大致可劃分為兩個大上升周期;當然在這兩個大上升周期內,樓價亦會出現調整,惟幅度不會多於兩成。而在這兩個上升大周期中,大型單位在「上升大周期1」的升幅明顯較突出;反之,小型單位在「上升大周期2」的表現則較佳。

另外,截至目前為止,「上升大周期1」和「上升大周期2」的實質(即扣除通脹)升幅和周期持續的時間相若(註:「上升大周期2」尚未確認見頂)。若然自2003年至今上升周期的實質升幅和維持的時間可媲美「上升大周期1」,意味目前樓市的升勢已差不多達標。不過,世事又豈會這麼簡單地重複?無論如何,參考「上升大周期1」完結的導火線──亞洲金融風暴外來因素,以及過去8年樓市升勢催化劑,很大程度上受到資金湧入所造成。故此,觸發「上升大周期2」完結的導火線,相信仍然是來自外在衝擊的因素。至於是什麼的外來衝擊因素呢?你話呢?